Behind Guming's Restart of IPO: The Older It Gets, the More "Profit Is King".

Author | Yang Yafei

Editor | Qiao Qian

"The third new tea drink stock" is still on the way.

After the initial listing application expired earlier this year, Guming has recently made another attempt to go public. According to the documents submitted to the Hong Kong Stock Exchange, Guming updated its prospectus on December 15. Not long ago, the China Securities Regulatory Commission disclosed that this tea drink brand has completed the filing for listing in Hong Kong and plans to issue no more than 441 million ordinary shares. In addition, Xiaocaiyuan also passed the Hong Kong stock listing hearing recently. The long-silent catering IPO market may be heating up again.

This prospectus is the best window to observe the current tea drink market. Whether in terms of GMV or the number of stores, Guming ranks second in the industry. The average customer transaction value of Guming is between 10 and 18 yuan, which is a red ocean market with the most brands and the fiercest competition. In addition, most of Guming's stores are located in the lower-tier markets, with similar sales proportions of milk tea and fruit tea, and it has also entered the popular coffee track.

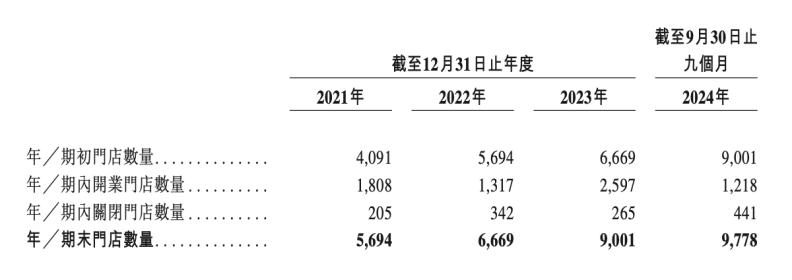

This year, Guming still maintains a growth trend. According to the prospectus, Guming's GMV in the first three quarters of 2024 was 16.6 billion yuan, a year-on-year increase of 20.4%, and the corresponding number of stores was 9,778, just one step away from reaching 10,000 stores.

However, the growth rate of store expansion has significantly slowed down this year. Only 777 new stores were added in the first three quarters, with an average monthly net increase of 86.3 stores, far lower than the average monthly net increase of 194.3 stores last year.

Guming once shouted the slogan of "10,000 stores" last year. In fact, the company did not pursue the absolute value of store growth this year but hit the brakes. The number of new stores opened in the first three quarters of this year is less than half of that of last year. Moreover, the ratio of store openings to closings was 9.8:1 in 2023, but it has changed to 2.76:1 in the first three quarters of this year.

One of the reasons for the slowdown is that the growth of same-store GMV has already slowed down.

Excluding the two major markets of Fujian and Jiangxi, in the first three quarters of 2024, the same-store GMV of Guming in core cities declined slightly, resulting in a slight 0.7% drop in the overall same-store GMV nationwide. Last year, this indicator was 9.4%. Of course, last year's high growth was partly based on the special market situation in 2022. However, it is an undeniable fact that the same-store growth has slowed down this year during the expansion process.

This is the first time in the past four years that Guming has experienced a negative growth in same-store GMV, and the negative effects of rapid expansion are beginning to show. The positive feedback from the slowdown is that the profit level has been maintained.

In the first three quarters of 2024, Guming's adjusted profit was 1.15 billion yuan, an increase compared to 1.04 billion yuan in the same period last year. The corresponding operating profit margin was 20.9%, although it decreased by 2.3 percentage points compared to the same period last year, it is still significantly higher than the industry average of 10% - 15%.

Rather than reaching the milestone of 10,000 stores, they prefer to maintain the profit ability of existing stores.

A Year of Slowing Growth for the Industry

For the new Guming franchisees who joined in 2024, this year they have to face greater competitive pressure.

According to the prospectus, in the first three quarters of 2024, the average GMV per order and the average daily order quantity of Guming both slightly declined. This ultimately reflects in the fact that the average daily GMV of each new franchise store has decreased from 5,800 yuan in the same period last year to 5,200 yuan.

The price war in the milk tea industry has intensified significantly this year. Chawangting is the biggest variable this year. After they made fresh milk tea popular, Guming and Luckin followed suit with a 9.9 yuan offer. Luckin directly continued the 9.9 yuan subsidy, and Guming once reduced the price of its fresh milk tea series products to 9.9 yuan.

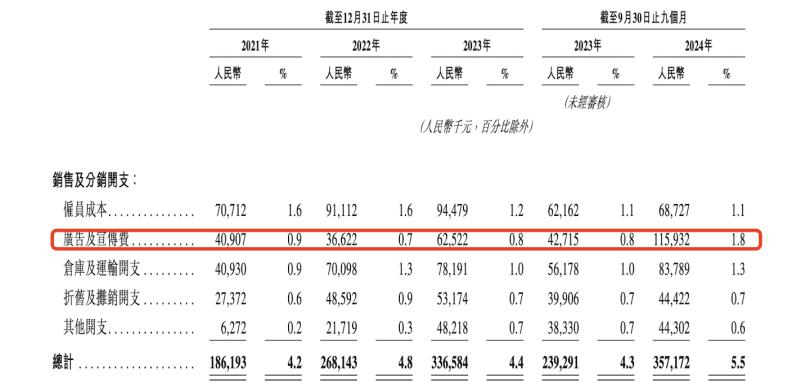

Guming spent more money on marketing this year. The expenditure on sales and distribution accounted for 5.5% of Guming's sales revenue in the same period this year, up from 4.3% in the first three quarters of last year. Among them, the biggest variable comes from the advertising and promotion expenses, which accounted for 1.8% of the revenue, a significant increase from 0.8% in the first three quarters of last year, with the amount exceeding 110 million yuan.

Under the fierce price war, not everyone can survive this summer. The first-tier franchisees are the first to feel the change in the market. In the first three quarters of this year, the churn rate of Guming franchisees reached 11.7%, compared to 8.3% for the whole of last year, and only 6.7% in 2022, which was affected by the epidemic.

Guming is not an isolated case. In the entire milk tea and beverage industry, a shakeout is also accelerating this year. According to data from Zhaimen Canyan, as of November 12, there are approximately 413,000 milk tea and beverage stores nationwide. Nearly 142,000 new stores have been opened in the past year, while approximately 18,000 net stores have been closed. That is to say, approximately 160,000 stores have been closed in the past year.

Before this, the overall number of tea drink stores was still in net growth. According to Zhaimen Canyan's statistics, excluding coffee specialty stores, from 2023 to March 2024, the number of operating tea drink stores in China was approximately 413,000. During this period, approximately 230,000 new stores were opened, and approximately 221,000 stores were closed, with a net increase of 8,272 stores.

There are several reasons for the current red ocean situation. The tea drink industry is already obviously saturated, shifting from an incremental to a stock market. The trend of coffee and milk tea integration, along with the 9.9 yuan price war, has also taken a share of the milk tea market. For some people, both coffee and milk tea are just a flavorful drink.

It is not only Guming that has adopted a more conservative store opening strategy. Previously, Heytea mentioned in an internal letter to its partners that it will not pursue the short-term speed and quantity of store openings, but rather focus on the quality of store openings and operational quality.

Mixue Bingcheng, which has the largest number of stores, has also seen a slowdown in its scale growth and recently raised the retail prices of its products in some areas of Beijing, Shenzhen, and Guangzhou by 1 yuan. This is their second price increase this year. Previously, in March this year, Mixue Bingcheng raised the prices of its products in some areas of Shanghai by 1 yuan.

In 2023, with the expansion pace, Guming's gross profit and operating profit margin increased simultaneously. But in the past year, when the market trend turned downward, only one of expansion and profitability could be chosen. And maintaining profitability has become the common choice of the leading brands.

From Fruit Tea to Milk Tea, the Tea Drink Industry Shakeout Will Accelerate

Against the backdrop of a slowing growth rate, Guming's expansion focus is further "downward". In 2021, the proportion of its stores in second-tier and lower-tier cities had already reached 78%, making it the brand with the highest proportion among the top 5. By the first three quarters of this year, this proportion has further increased to 80%.

Judging from the newly added stores, the lower-tier cities in the lower-tier markets are the focus of expansion. In the first three quarters of this year, the number of stores they opened in third- and fourth-tier cities and below was the largest, accounting for 70% of the new stores this year.

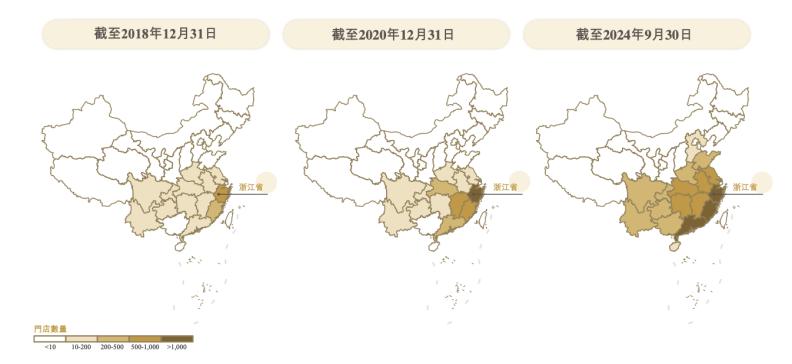

Behind this high proportion is Guming's strategy of opening more stores in a concentrated area. Unlike other leading tea drink brands with a national layout, Guming's store network presents a typical single-center structure. It continues to intensify its presence in its base in Zhejiang and expands to the surrounding areas. Most of its stores are located in the central and eastern markets such as Fujian, Jiangxi, Guangdong, Hubei, Jiangsu, Hunan, and Anhui. It is also the only regional brand among the leading ones and has not yet opened stores in Beijing and Shanghai.

The proportion of stores in rural towns is also relatively high. As of 2023, the proportion of Guming's stores in rural towns reached 38%, and by the first three quarters of this year, this proportion has increased to 40%.

This intensification measure is to maximize the efficiency of its cold chain. Compared with cooperative social logistics, the advantages and disadvantages of self-built cold chain are obvious. Warehouse distribution is more controllable, but the cost is relatively fixed, and the efficiency improvement can only rely on the continuous increase of the regional density of its own business.

Taking Zhejiang as an example, 94% of the stores in the region are within the 150-kilometer radiation range of its warehouse. 97% of its stores nationwide can achieve a cold chain delivery frequency of once every two days.

The high proportion in the lower-tier markets, the early layout in the cold chain, and the price range of 10 - 18 yuan determine that Guming is taking the route of upgrading the consumption of tea drinks in the lower-tier markets. However, the main product line has also been changing in recent years following the market trends.

In 2021, Guming's largest category was still fruit tea, including Cheese Grape, Cheese Peach, Perfume Lemon, and Full Cup Bayberry, etc. At that time, fruit tea accounted for 44% of the total cups sold, milk tea accounted for 39%, and coffee and other beverages accounted for 17%.

At that time, Chawangting was still a regional internet-famous brand, and fruit tea was the popular category in the market, represented by Heytea and Nayuki. The latter successfully went public in 2021 and became the "first new tea drink stock". However, at that time, they did not offer franchises and their stores were concentrated in first- and second-tier cities. Guming quietly started its business in the lower-tier markets.

In the past two years, with the rise of milk tea, the proportion of milk tea in Guming's products has gradually increased. The sales proportion of milk tea beverages has gradually increased from 39% in 2021 to 47% in the first three quarters of 2024, with a sales volume of 466.8 million cups during this period.

From Heytea to Chawangting, Guming, the second in the industry, has not missed the popular trend categories of tea drinks.

The layout of coffee is also expanding. Previously, 36Kr reported that the number of Guming's coffee product stores has expanded from 500 in September to over 2,000 last month.

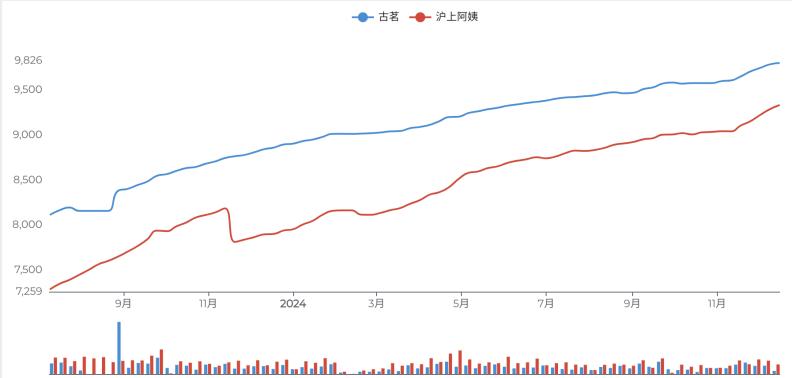

In terms of scale, it is still undetermined who will be the next to reach 10,000 stores. The closest contender is Hushang Ayi. According to Jihai Brand Monitoring, the latest number of Hushang Ayi stores has reached 9,333, and the store growth rate in the last quarter was higher than that of Guming.

The changes in the number of stores of Guming and Hushang Ayi in the past year, according to Jihai Brand Monitoring

Unlike Chawangting, which expands rapidly with its popular fresh milk tea product, Hushang Ayi focuses on the fresh fruit tea track. It directly adds the suffix "Fresh Fruit Tea" to the online store names to increase product recognition and recently launched a series of fruit and vegetable tea products.

The tea drink business targets young people, and the theme of trying new flavors remains unchanged. Because of this, the tea drink industry has a typical fashion risk. There has also been a debate in the industry about whether fresh milk tea or fresh fruit tea better represents the industry trend. However, both the product and the price range are already crowded enough.

In the trend of stock market shakeout, the tea drink market will obviously further concentrate on the leading brands. In addition to Guming, a number of leading brands such as Hushang Ayi, Chawangting, and Chayanyuese have also been rumored to be making a new push for an IPO. And the real valuation differentiation will be more reflected in the ability to make profits.