Die Robotikbranche in ständiger Veränderung: Die Entwicklungsschlüssel hinter den Halbjahresergebnissen der A-Aktien im ersten Halbjahr 2025

The recently held 2025 World Robot Conference has once again pushed the popularity of robots to a new high.

More than 200 domestic and foreign robot companies participated in the conference, displaying over 1,500 robot products, making it the largest - scale exhibition in history. Among the over 200 companies, 50 are engaged in the production of humanoid robots, indicating that the industrial scale of embodied intelligent robots is taking shape.

The booming humanoid robot industry has directly boosted the performance of related companies in the sector. According to Flush iFinD data, among the 44 humanoid robot - related companies that have released semi - annual performance forecasts, 25 have reported "substantial increases" in performance, 7 have "pre - increased", and 12 have "turned losses into profits". No company has clearly shown a loss, and the overall performance of the sector is very positive.

The rising market of the humanoid robot industry chain is a macro - level manifestation. At the micro - level, factors such as the accelerated penetration of new energy vehicles, the recovery of the consumer electronics market, and the upgrading of intelligent manufacturing equipment have directly driven up the main business income, which is the main reason for the outstanding performance of most companies in the humanoid robot sector.

Are all companies in the humanoid robot sector expected to have good news? Each has its own joys and sorrows

The explosion of the humanoid robot industry has a certain inevitable relationship with the development of the new energy vehicle industry. In terms of industrial structure, the underlying structures of intelligent vehicles and intelligent robots are basically the same, both being a combination of hardware and software. It can be said that current new energy vehicles can be regarded as humanoid robots operating in the guise of new energy vehicles. Many companies currently engaged in the production of humanoid robot components were originally automobile component manufacturers.

Image source: Taotao Auto official WeChat account

For example, Taotao Auto (301345), whose main business is intelligent electric low - speed vehicles and special vehicles, announced on June 30 that it expects its net profit attributable to shareholders of the listed company in the first half of 2025 to be between 310 million yuan and 360 million yuan, a year - on - year increase of 70.34% - 97.81%. On June 27, it announced through its official WeChat account that the first prototype of the humanoid robot (K - Scale humanoid robot K - Bot) manufactured by Taotao Auto was successfully rolled off the production line, marking a key progress in its entry into the cutting - edge field of humanoid robots.

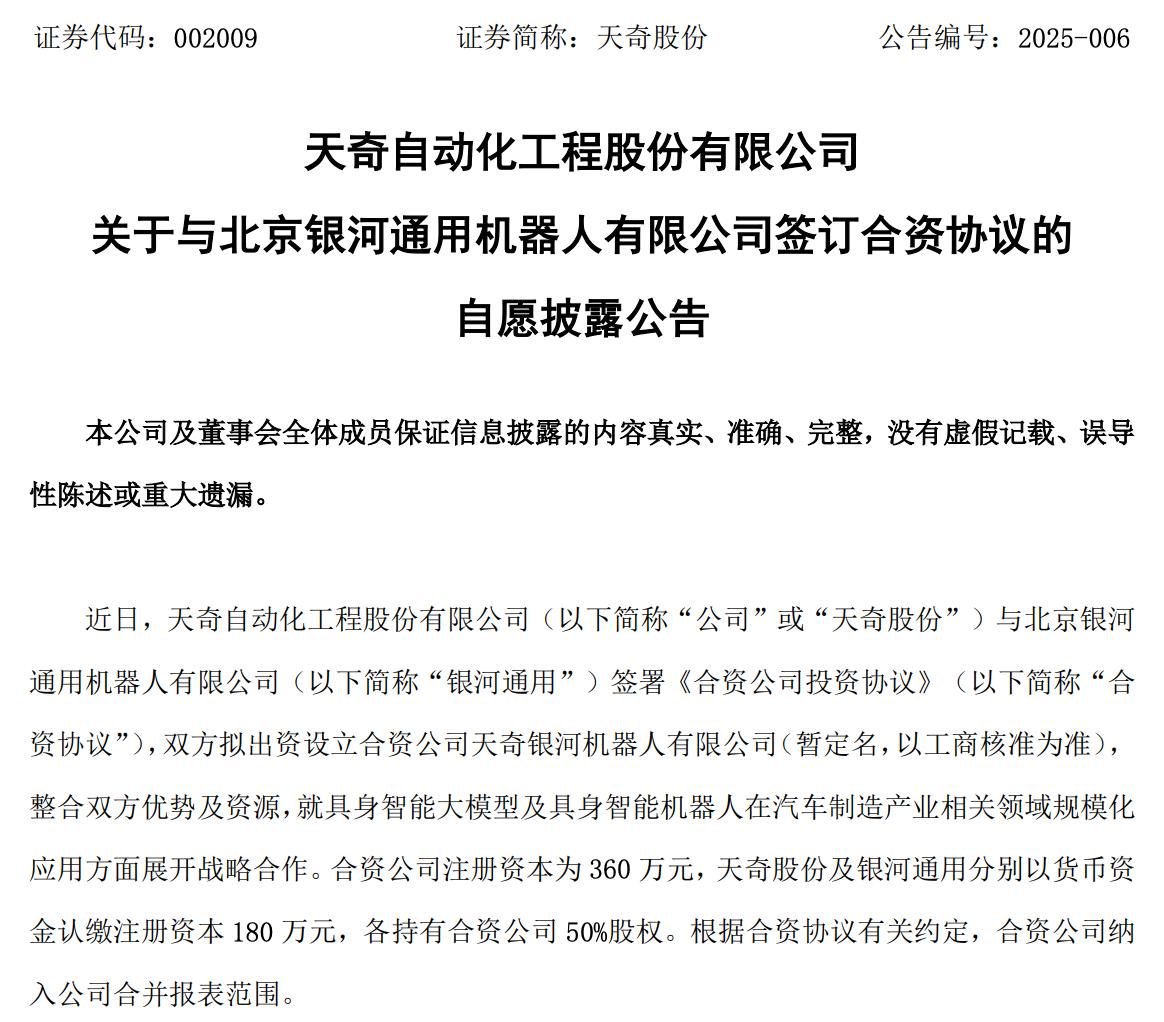

Tianqi Co., Ltd. (002009), which focuses on intelligent equipment and lithium - battery recycling business, also released a semi - annual performance forecast on July 15, expecting to achieve a non - recurring net profit of 12 million - 16 million yuan. Compared with a loss of 81.3086 million yuan in the same period last year, it is expected to turn losses into profits.

As early as February, Tianqi Co., Ltd. signed an "Investment Agreement for a Joint - Venture Company" with Beijing Galaxy General Robot Co., Ltd. and plans to contribute capital to establish a joint - venture company, Tianqi Galaxy Robot Co., Ltd. The business direction of this company is to develop and apply embodied intelligent robots in industries related to automobile manufacturing, etc., and it is expected to achieve mass delivery starting from 2025.

On the other hand, with the recovery of the consumer electronics market and the increasing demand for various electronic products, the demand for some components or technologies related to humanoid robots, such as sensors, chips, transmission components, and precision workpieces, has also increased. The reduction in the cost of these components provides a better foundation for the R & D and production of humanoid robots and also reduces the production cost of humanoid robots.

The semi - annual performance forecast of Lianchuang Electronics (002036), an optical and optoelectronic enterprise, shows that it expects its net profit attributable to the parent company in the first half of 2025 to be between 18 million yuan and 26 million yuan. In the same period last year, it had a loss of 64.9914 million yuan; the non - recurring net profit is expected to be a loss of 26 million - 45 million yuan, compared with a loss of 99.9637 million yuan in the same period last year, successfully turning losses into profits.

Lianchuang Electronics said that during the reporting period, its core optical business developed smoothly, the in - vehicle optics continued to grow, and the touch - display industry completed the adjustment of customer and product structures, improving production efficiency. In addition, during a roadshow event at the beginning of 2025, Lianchuang Electronics said that its lens and module products can be applied to humanoid robots. Moreover, Lianchuang Electronics believes that the overall scale of its touch - display business and mobile phone optical business will continue to shrink in 2025.

The promotion of the performance of humanoid robot - related companies by the upgrading of intelligent manufacturing equipment is also obvious. Although these upgrades may not directly affect the humanoid robot ecosystem itself, their impact on corporate performance cannot be ignored.

Pengding Co., Ltd. (002938), which has been deeply involved in the PCB business, expects that from January to June 2025, its net profit attributable to shareholders of the listed company will be between 1.198 billion yuan and 1.26 billion yuan, a year - on - year increase of 52.79% - 60.62%; the net profit after deducting non - recurring gains and losses will be between 1.105 billion yuan and 1.161 billion yuan, a year - on - year increase of 46.12% - 53.61%.

In addition to "continuously controlling costs and improving manufacturing processes", Pengding Co., Ltd. specifically mentioned the impact of "strengthening automated production" on reducing production costs and increasing profits.

Although the above factors cannot cover all companies in the humanoid robot sector, it must be admitted that the label of the humanoid robot sector has indeed changed the market expectations and growth logic of related companies and has also greatly contributed to the improvement of their performance.

Comparing with new energy vehicles, humanoid robots will eventually face potential hidden dangers

The performance changes of humanoid robot - related companies are indeed worth looking forward to. However, 2025 is only the upward stage after the humanoid robot industry entered the explosive period. After continuous investment and financing to cultivate the industry chain and gradually enter maturity, the humanoid robot industry will also enter a reshuffle period. At that time, the problems in the industry chain will be exposed one by one, and these problems masked by the development environment are the real challenges that the humanoid robot industry will face.

As mentioned before, there is not much difference between new energy vehicles and intelligent robots at the industrial level. Both are combinations of hardware and software, just realizing different functions. In recent years, the penetration rate of new energy vehicles has been continuously increasing, and the industry has gradually entered a reshuffle period. By referring to the development cycle of the new energy vehicle industry, to a certain extent, we can benchmark the subsequent development process of the humanoid robot industry, and then make reasonable predictions about the potential problems, so as to see the development path of the humanoid robot track in the next few years.

Let's first look at the new energy vehicle track. At its peak, the number of new energy vehicle companies exceeded three digits, but now the number of active ones is no more than five. Many automobile brands that were once favored by the market, such as Aiways, WM Motor, Skywell, Zotye, HiPhi, Nezha, and Jiyue, have all failed. Even among the listed new - energy vehicle startups, only Li Auto achieved profitability in 2024, while NIO, XPeng, Leapmotor, and Zeekr are still in the quagmire of losses.

The rapid development of new energy vehicles and the short technology iteration cycle have forced vehicle manufacturers to maintain high R & D expenses for a long time. In order to compete for market share, they have to compete in both R & D and marketing, and the sales expenses are also high. If we add various expenditures in the overseas market, the financial situation of vehicle manufacturers has been far from satisfactory for a long time.

Currently, the humanoid robot industry seems to be following the old path of new energy vehicle companies. However, as a more technology - intensive industry, the current humanoid robot industry is even more prominent than the new energy vehicle industry at the same stage. Firstly, there are still uncertainties or technical bottlenecks in some fields such as operating systems and machine vision, and companies still need to invest resources to continuously tackle these problems.

In addition, the supply of components and raw materials involved in robot production is more complex. The yield rate of any component and the price fluctuations of required raw materials will be quickly transmitted to the humanoid robot track. Especially against the backdrop of increasing global economic uncertainties, the instability of the supply chain has further increased, and neither the entire industry nor individual companies can stay out of it.

At the same time, the humanoid robot companies are currently developing rapidly. Referring to the cycle of new energy vehicle companies, it is expected that in about three years, the humanoid robot industry may face its "ChatGPT moment" and enter a cruel reshuffle period. How many companies that enter the market at this time will still remain is still unknown.

Of course, it is not excluded that the reshuffle may be caused by the early strengthening of collaborative development among companies in the industry chain. A closer cooperative relationship will be formed among component suppliers, robot manufacturers, system integrators, and application companies to jointly promote the innovation and application of robot technology. In particular, humanoid robots can rely on new energy vehicle companies to form an industry development paradigm of "automobile + robot". 4S stores may sell both cars and robots.

Currently, the performance forecasts of A - share robot - related listed companies only reflect the current development status of the industry. Although the performance of companies in the industry chain is expected to be good at this stage, challenges such as intensified market competition, R & D pressure, and supply - chain risks are always looming and will arrive at an accelerating pace. The continuous expansion of application scenarios, the continuous improvement of intelligence levels, and the strengthening of industrial collaborative development may be the few ways for humanoid robot companies to maintain continuous growth.

This article is from the WeChat official account "GPLP", author: Ma Hehuan. Republished by 36Kr with permission.